February 28, 2024

-1.png)

Want to keep your finances on track? Following a budget is the first step. We'll teach you how to create one. Don't let the fear of not knowing where to start keep you from creating a budget that will keep your finances on track.

It's no secret that a budget is the key to eliminating financial stress and reaching your financial goals. So why do so many of us fail to follow one? Maybe you're uncertain as to why a budget is necessary and think you can keep track of your spending other ways. Or maybe you've never created a budget before and the enigma of it scares you to death. Either way, at Education First Federal Credit Union, we are committed to helping you achieve financial success and are here to walk you through the steps.

What is a Budget?

A budget may sound like a scary word - one that conjures images of your living an austere and joyless life - but at its core it is really a quite simple tool that will help ensure you have enough money to cover all of your expenses. A personal budget boils down to three things: Income - Expenses - Savings.

Why You Need a Budget

A well-crafted budget is not only valuable but also essential for maintaining financial stability. It empowers you to effectively manage your money and make significant progress towards your personal and financial goals.

Budgeting is a must when it comes to your personal finances. It helps you to exercise control over your money and ensures that you have a clear understanding of your income, expenses, and savings goals. This awareness lets you make informed decisions about your finances and helps you prioritize your spending. Without this knowledge, it's easy to find yourself in a cycle of overspending and even digging yourself into an ever-deepening hole of debt.

How to Create a Budget

Creating a budget isn't hard, but it does require you to put in some work on the front end. Below we outline the basic steps that will help you to build your budget.

1. Set Clear Goals

Setting clear financial goals is an essential step in creating a budget. Think about what you want to achieve in the short- and long-term. Your goals might include paying off debt, building up your emergency fund, saving for a down payment on a house or putting your kids through college. Short-term goals should take around one to three years to achieve and might include things like setting up an emergency fund or paying down credit card debt whereas Long-term goals might be saving for retirement or paying for your child's college education. And whether those goals are 13 months or 13 years, this is an important step as having clear goals can help to motivate you to stick to your budget.

2. Calculate Your Income

The foundation of an effective budget is to know your net income. Whereas Gross Pay refers to the total amount of money you earn before any deductions are taken out, Net Income is the wages that you take home after deducations for taxes or employer sponsored plans, like a 401k and health insurance. Depending on your stage and place in life, these deductions can also include child support or other court ordered payments. This is why when you are creating a budget it's important not to focus on your salary or hourly wage as it could be misleading about how much money is truly available to you and can help you reach your financial goals.

If you work as a freelancer, contractor, or are self-employed, it's crucial to be honest with yourself about the stability and regularity of your income sources. Keeping detailed records of your contracts and payments can help you effectively manage any fluctuations in your income.

3. Track Your Spending

Once you know how much money you have coming in, the next step is to figure out where it’s going. Tracking and categorizing your expenses is crucial as it will help you to determine what you are spending the most money on and where it might be easiest to save.

A great place to start tracking your cashflow is to view your credit card and bank transactions online as they show spending in real time. Education First members can use iThrive, our free online budgeting software that connects directly to your checking account. Then you can create categories and assign transactions by type, seller, or keyword, making it easier to track in the future. You can also track your cash flow and spending by category, set up savings goals and more! Or if you just don't love technology, there's always the option of going old school and utilizing this free budget worksheet download.

As you go about this task, it is important to categorize your spending into Fixed and Variable Expenses. Fixed Expenses recur regularly - usually monthly - and include things like rent or a mortgage payment, utilities, insurance, auto loan payments and any other debt you are paying off. Next list your variable expenses. Variable expenses are those that may change from month-to-month and include items like groceries, gas and money spent on entertainment or hobbies.

4. Do the Math. Make a Plan.

The next step is the part that can be scary but is crucial for a successful budget. This step requires that you take all that data about your expenses and spending for the last 60-90 days and subtract that from your net income for the same period. This will give you an honest look at how much money comes in and how much is going out. Then compare that to your net income and priorities. Consider setting specific—and realistic—spending limits for each category of expenses.

Breaking down your expenses into necessities and desires can provide valuable insight into your spending habits. For example, while gasoline for your daily commute is a necessity, a monthly music subscription may fall under the category of luxury. This distinction is crucial when determining how to reallocate funds towards your financial objectives.

Creating a realistic budget involves allocating your income towards your expenses and goals in a way that is sustainable and achievable. Start by listing all your sources of income and the amount you earn from each source. Then, list all your expenses, including both fixed and variable expenses.

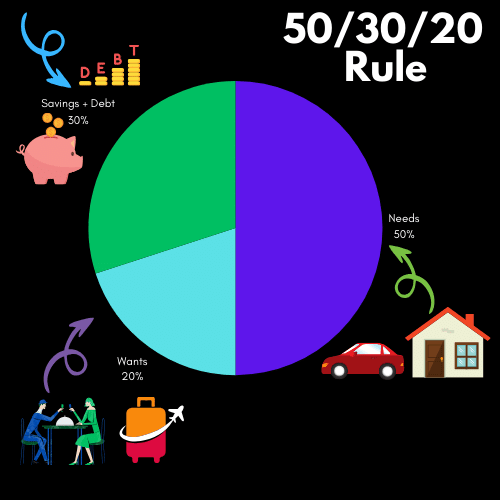

Next, prioritize your expenses based on your financial goals. Allocate a portion of your income towards needs, wants and savings or debt reduction. An effective way to do this is by using the 50/30/20 budget rule. This rule states that you should spend up to 50% of your after-tax income on needs and obligations that you must have or must do. The remaining half should be split between savings and debt repayment (20%) and everything else that you might want (30%).

It is important to be realistic about your budget and not allocate more money than you have. Be prepared to adjust as needed and be flexible in your spending. Remember, a budget is a tool to help you achieve your financial goals and should be tailored accordingly.

5. Build in Flexibility.

While it is important to stick to your budget, it is also crucial to build in some flexibility. Unexpected expenses or changes in your financial situation may arise, and having some room for adjustments can help you more easily navigate these tough times.

One way to create flexibility is by creating a separate category in your budget for unexpected expenses or emergencies. Allocate a certain amount of money each month towards this category, so you have a safety net in case something unexpected happens.

By building in flexibility, you can ensure that your budget remains realistic and achievable. It allows you to adapt to unexpected circumstances without derailing your financial progress.

6. Review and Adjust.

It is important to review and update your budget regularly. As your financial situation changes (income and/or expenses) and your goals evolve, your budget will require adjustments. Be prepared to embrace change and maintain a flexible mindset when it comes to budgeting. This may involve reassessing some of your "wants." If you've already adjusted your discretionary spending, delve deeper into your monthly expenses. Upon closer examination, you may discover that a supposed "need" is actually a "want" that is just hard to let go of.

If the numbers still aren’t adding up, look at adjusting your fixed expenses. Could you, for instance, save more by shopping around for a better rate on auto or homeowners insurance? Such decisions come with big trade-offs, so make sure you carefully weigh your options. If you find that your budget isn't quite balancing out, consider tweaking your fixed expenses. Have you explored the possibility of trading in your auto for a less expensive model, or comparison shopping for a discount on insurance? While these choices may take some time or involve some trade-offs, it's important to weigh them carefully if they hold the potential to improve your financial well-being.

Don't underestimate the impact of small savings - they can really add up over time. Making even minor adjustments can lead to significant extra money in your pocket.